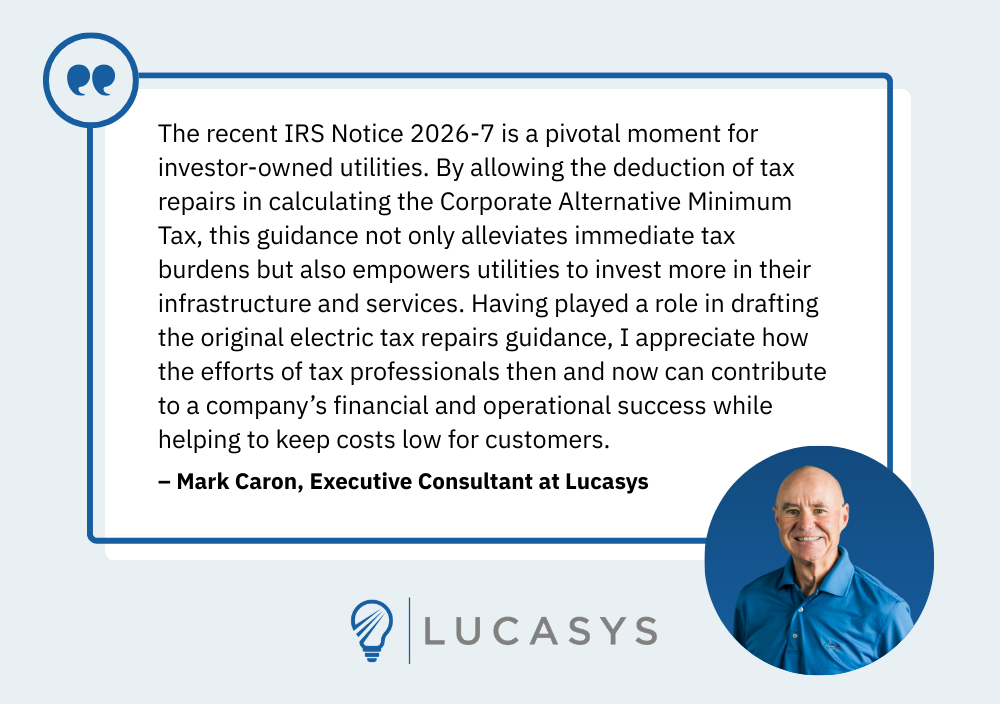

Recent IRS Notice 2026-7: Impacts on Corporate Alternative Minimum Tax for Investor-Owned Utilities

In a significant development for corporate taxpayers, the IRS has released Notice 2026-7, providing additional interim guidance on the application of the Corporate Alternative Minimum Tax (CAMT). This guidance is particularly relevant for investor-owned utilities that are subject to the CAMT due to their financial statement income exceeding $1 billion.

Key Takeaways from IRS Notice 2026-7

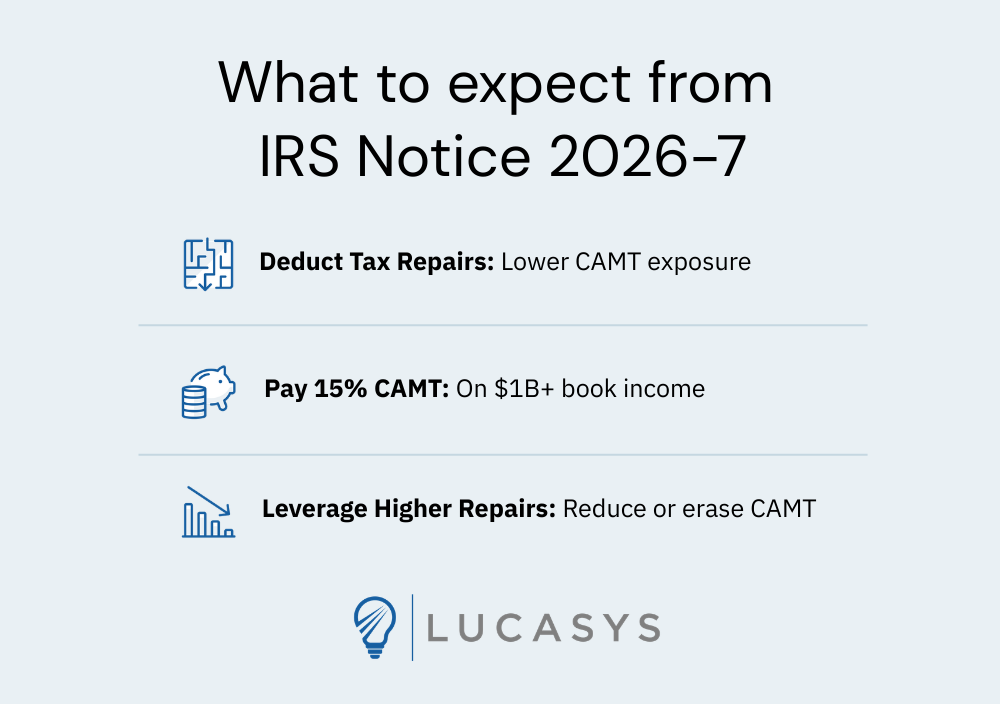

Deduction of Tax Repairs: The most noteworthy aspect of the new guidance is that it allows taxpayers to deduct tax repairs when calculating CAMT. This is a crucial change, as it directly influences the tax obligations of affected corporations.

Understanding CAMT: The CAMT is imposed on corporate taxpayers with a history of financial statement income exceeding $1 billion. Once a corporation is subject to this tax, it must pay 15% of its book income, which can significantly impact its overall tax liability.

Impact on Investor-Owned Utilities: A number of investor-owned utilities fall under the CAMT umbrella. The allowance to deduct tax repairs, which are often significantly higher than book repairs, will substantially lower or potentially eliminate their current year’s CAMT liabilities. This change is expected to provide considerable financial relief to these companies.

Understanding Tax Repairs

Tax repairs play a critical role in the financial landscape for corporations, particularly for those subject to the Corporate Alternative Minimum Tax (CAMT). Here’s a closer look at what tax repairs entail and their significance:

What Are Tax Repairs?

Definition: Tax repairs refer to expenditures that qualify for immediate deduction under the Internal Revenue Code (IRC) rather than being capitalized and depreciated over time. These expenses typically involve maintaining or restoring property rather than improving it.

Comparison with Book Repairs: Unlike book repairs, which are recorded based on Generally Accepted Accounting Principles (GAAP), tax repairs allow for a more aggressive treatment of repairs and maintenance costs. This difference often results in a higher deduction for tax purposes compared to financial reporting.

Impact on Investor-Owned Utilities

Deductions Under CAMT: With the recent IRS guidance, investor-owned utilities can now deduct these tax repairs when calculating their CAMT. This is particularly beneficial because these deductions can significantly exceed the amounts reported under book repairs.

Financial Relief: The ability to deduct tax repairs reduces the taxable income subject to the 15% CAMT, potentially eliminating or drastically lowering tax liabilities for utilities with substantial repair expenditures. This financial relief can free up resources for critical investments in infrastructure, technology, and service enhancements.

Strategic Considerations

Tax Planning: Companies should consider incorporating tax repairs into their tax strategy, especially in light of the new IRS guidance. Understanding the nuances between tax and book repairs can lead to substantial tax savings.

Documentation: Proper documentation of repair expenditures is essential to substantiate tax deductions and withstand potential audits. Keeping detailed records will ensure compliance and maximize the benefits from tax repairs.

Conclusion: A Positive Shift for the Utility Sector

The IRS's Notice 2026-7 is a significant development for investor-owned utilities, offering them a pathway to reduce their tax burdens significantly. This adjustment not only enhances their financial standing but also allows for greater investment in infrastructure and services. Customers could also see benefits as some companies were successful in obtaining regulatory approval for recovering CAMT in some fashion which would have increased customer rates.

For more details, refer to the official IRS Notice here. To schedule a Tax Repairs discussion with a trusted Lucasys expert, book a meeting here.

How Lucasys Can Help

Lucasys delivers Tax Repairs software, and other technology-enabled services to empower finance, accounting, and tax professionals in asset-intensive industries to optimize the financial performance of their fixed assets and proactively meet changing regulatory and compliance requirements. With a core focus on rate-regulated utilities, Lucasys provides the industry and domain expertise energy and utilities require to meet their business objectives. To learn more about Lucasys, visit https://www.lucasys.com or follow us on LinkedIn.