Lucasys Blog

Mastering ASC 740: Best Practices for Utility Companies

ASC 740, or Accounting Standards Codification 740, governs how companies report income taxes in their financial statements. For utility companies, complying with ASC 740 presents unique challenges due to the industry's complex regulatory environment and the intricate nature of tax provisions, deferred taxes, and rate-regulated accounting practices. Mastering ASC 740 is essential for ensuring accurate financial reporting, mitigating risk, and satisfying both regulatory and audit requirements.

Navigating Tax Challenges in a Multi-Jurisdictional Utility Operation

For investor-owned utility companies operating across multiple states, managing tax compliance is a complex and often daunting task. Each state has its own set of tax laws, regulations, and reporting requirements, which can create a labyrinth of obligations for utility tax departments. In this environment, staying compliant while optimizing tax positions requires not only deep expertise but also the right tools and technology.

Strengthening Infrastructure for Resilience: The Crucial Role of Tax Software in Investor-Owned Utility Companies

As climate change accelerates, extreme weather events are becoming increasingly common, posing significant challenges to utility companies across the globe. Investor-owned utilities (IOUs), responsible for providing essential services to millions, are at the forefront of efforts to strengthen infrastructure and ensure resilience against these threats. While physical upgrades and operational strategies are crucial, one often-overlooked aspect of this resilience is the role of a utility’s tax division and its technology. Robust tax management is vital in funding, maintaining, and expanding resilient infrastructure.

Corporate Tax Rate Changes on the Horizon… Again! What Utilities Need to Know

As the 2024 election season gains momentum, regulated utilities are facing the prospect of significant policy shifts that could dramatically impact their financial landscapes. Vice President Kamala Harris has recently announced that if elected, she plans to raise the corporate tax rate to 28%. This proposal has raised alarms among tax leaders and CFOs within the utility sector, as the potential changes could lead to substantial adjustments in deferred tax liabilities.

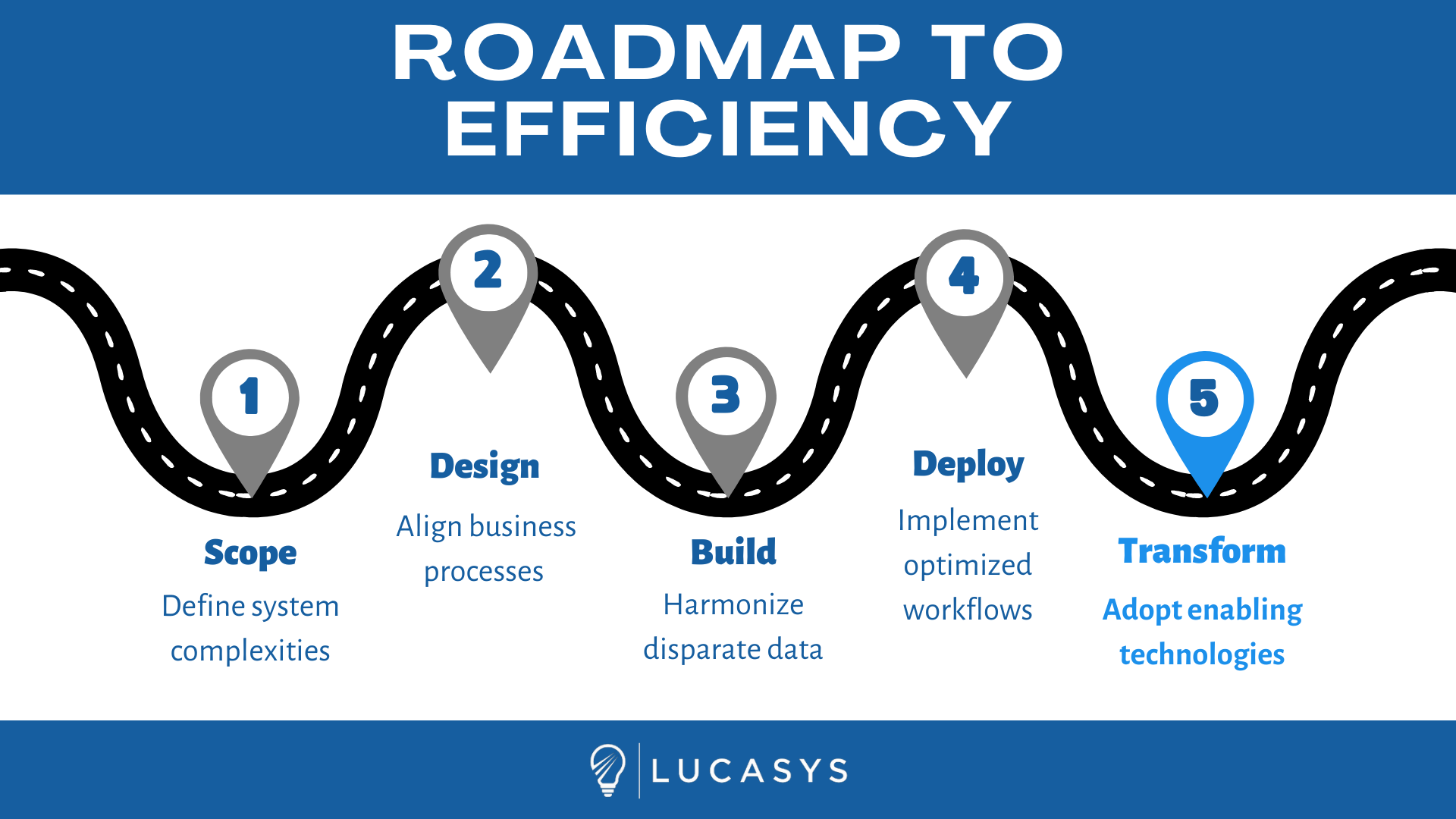

Innovation in Tax Fixed Assets: Hope Utilities Adopts Best-in-Class Lucasys Software

Leading natural gas and water distribution services company, Hope Utilities, has implemented Lucasys’ industry-leading tax fixed asset software. Faced with the challenges of maintaining legacy software systems, Hope Utilities recognized the opportunity to streamline their accounting solutions and transform their business processes.

AEP's Data Revolution: Partnering with Lucasys to Prepare for the Next Leap in Tax Technology

American Electric Power (AEP), one of the nation’s largest utility power producers and operator of the nation’s largest electric transmission network, has a longstanding reputation as an industry leader in digital transformation and technological innovation. Successful operations have led AEP to sustained growth, expanding the organization into additional states and service territories while accumulating a blend of data, processes, and technologies.

Summit Utilities Partners with Lucasys to Streamline Tax Fixed Assets

In a pivotal move towards operational efficiency and advanced technology adoption, leading natural gas company Summit Utilities has embarked on a transformative endeavor with premier software and consulting firm Lucasys to revolutionize their tax fixed asset software.

IRS Issues New Safe Harbor Rules for Natural Gas Repairs: What Rate-Regulated Utilities Need to Know

The IRS has issued a new revenue procedure, Rev. Proc. 2023-15, providing a safe harbor method of accounting for natural gas transmission and distribution property repairs, maintenance, replacements, and improvements. This new method allows taxpayers to classify these costs as either capital or deductible expenditures, providing clear and bright-line rules to reduce the burden of compliance.

Proposal to Increase the Corporate Tax Rate... Again!

In late March 2023, President Biden proposed a federal budget for fiscal year 2024 that will increase government spending in new infrastructure, education, healthcare, and climate change initiatives. To fund the investments, the Biden administration has proposed several tax reforms that will have important implications for corporations. Specifically, the proposed increase in the corporate income tax rate from 21% to 28% will have a significant impact on rate-regulated utilities

Details Emerge on Democrats’ Corporate Tax Rate Increase Proposals

Specifics for the “Build Back Better“ (BBB) reconciliation legislation have finally begun to emerge amid contentious intra-party debates within the Democratic caucus. The massive bill encompasses large portions of the Biden domestic political agenda, and debate is ongoing in Congress on the final scope of the bill and how its initiatives will be paid for.

Digital Technologies Propel Utilities to Transform Workforce

Utilities are bracing for a digital revolution, though according to a recent report most executives in the sector agree that their businesses are not prepared for it.

In the Digital Transformation and the Workforce Survey commissioned by EY Power & Utilities, nearly 90% of executives report having too few digitally savvy workers is frustrating their ability to adopt digital technologies. Not only is the problem of an insufficient workforce staring them in the face, by most of the respondents surveyed are lacking a plan on how to proceed. With near-universal agreement (94%) on the need for direct investment in technology and the workforce, utilities are soon to be left scrambling for solutions. The transformation of the power industry will be based on technology, but it will be driven by people.

Dueling Proposals: Which Plan Will Transform America's Infrastructure?

In March, the Biden administration unveiled a $2.3 trillion infrastructure plan which included many proposals that specifically target the energy industry, including expanded renewable energy tax credits, mandates for utility system modernization, and transitioning the power sector to emissions-free electricity by 2035. Congressional Republicans responded by releasing a $568 billion counter-proposal which included a more limited scope of what qualifies as infrastructure. Since that time Biden has offered to cut his plan to $1.7 trillion, and Republicans have countered again with second counter-proposal of $928B.

Cloud Computing is Revolutionizing Business Processes

Many industries are leveraging the power of cloud computing to revolutionize their processes, and the COVID-19 pandemic has further accelerated the need for software solutions that can be accessed remotely. Businesses are transitioning to more comprehensive digital processes with cloud solutions at their core.

Lucasys Announces Completion of SOC 2 Type 2 Audit Certification

Lucasys is proud to announce an important compliance milestone in the completion of a SOC 2 Type 2 attestation for its software solutions. This security compliance measure is a testament to Lucasys’ continued commitment to protecting customer data as it emerges as a leading cloud provider for enterprise financial solutions.

Lucasys Approved as CPE Sponsor by NASBA

Lucasys, a leading provider of cloud accounting, tax, and financial reporting solutions, today announced their certification registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education (CPE) on the National Registry of CPE Sponsors. Lucasys is certified to provide continuing education via group live and internet-based delivery methods.

Lucasys Sponsors EEI 2019 Financial Review

Lucasys is proud to partner with the Edison Electric Institute in sponsorship of the 2019 Financial Review, the organization’s annual report of the U.S. investor-owned electric utility industry.

Implications of 163(j) for utilities

On Monday, November 26, 2018, the Treasury Department published proposed regulations relating to section 163(j), as amended by the Tax Cuts and Jobs Act. For utilities with regulated operations (excepted trade or business) and non-regulated operations (non-excepted trade or business), the proposed regulations provide additional clarity regarding the applicability of the interest limitation on the consolidated group.